Indian markets ended lower for the week ended May 15, snapping the previous two weeks of gains. Selling in IT and banking stocks weighed on benchmark indices.

The NIFTY50 fell 2.2% to close at 23,643, while the SENSEX dropped 2.7% to 75,237.

The weakness was broad-based. All the major sectors ended the week lower, while Small-cap 250 and Mid-cap 150 indices fell 4.1% and 2.2%, respectively. This reflects that selling pressure was not limited to headline indices but also spread across the broader market.

The rupee added to the pressure, closing near 95.90 against the US dollar, its weakest level in 12 months. The sharp decline was seen due to elevated crude oil prices, a stronger dollar, and persistent FII outflows. The government’s decision to raise petrol and diesel prices by ₹3 per litre for the first time in four years further stoked inflation concerns and kept sentiment cautious.

Sectorally, the trend was weak with most indices closing in the red. IT stocks were the biggest drag, with the NIFTY IT index falling 5.7% for the week. Real-Estate (-8.1%), PSU Banks (-4.1%) and Automobiles (-4.3%) witnessed significant cuts. However, select defensive pockets like Pharma (+2.1%) and Metals (+1.9%) witnessed buying interest.

Spotlight: NIFTY IT remained under pressure this week as the global sell-off in software companies weighed on sentiment. U.S. and global tech names such as Cognizant and Accenture saw sharp declines. The concern is that AI tools may reduce the need for software products. This has made investors cautious on Indian IT companies. Going ahead, traders should watch whether IT heavyweights such as TCS, Infosys, HCL Tech and Wipro stabilise. Any recovery in the sector can support NIFTY, but continued weakness may cap the index’s upside. Against this backdrop, shares of LTIMindtree, Persistent Systems, Tech Mahindra and Coforge declined in the range of 6% to 8%.

️Key events in focus: The coming week will have light economic calendar. However, the spotlight will be on Nvidia, the world’s most valuable company, which will announce its results on Wednesday. Nvidia’s results will be closely tracked for cues on AI demand and data-centre spending. Any disappointment in guidance or margins could impact global risk sentiment.

Earnings blitz: The Q4 earnings season will continue to drive stock-specific action in India. Companies scheduled to announce results are Astral, Indian Oil Corporation, BEL, BPCL, PI Industries, Apollo Hospitals, Grasim, Aurobindo Pharma, GAIL, ITC, LIC, Max Health, Nykaa, Sun Pharma, Eicher Motors, Divi’s Laboratories and NTPC.

️Crude oil: Oil prices ended the week sharply higher as supply concerns around the Strait of Hormuz remained elevated. Brent crude settled at $109.26 per barrel, rising 7.9% for the week, while WTI crude settled at $105.42 per barrel, gaining 10% for the week. The move was supported by worries over limited flows through the Strait of Hormuz and tightening global oil inventories.

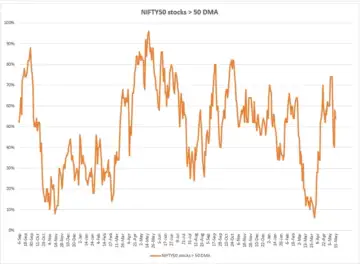

Market breadth

The percentage of NIFTY50 stocks trading above their 50-DMA dropped from around 74% to nearly 40%, reflecting broad-based selling pressure across index constituents. This is an important shift because breadth had improved strongly from the March lows, moving from deeply oversold levels near 5-10% to above 70% by late April. However, the latest fall suggests that participation has narrowed again and the market is no longer seeing the same broad support.

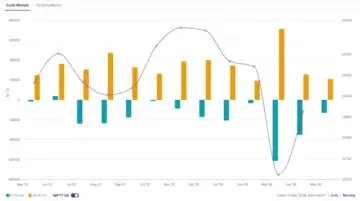

Foreign investors positioning

Foreign investors remained net sellers this week, having sold shares worth ₹13,583 crore. Foreign outflows from Indian equities have remained elevated this year, and the rupee’s weakness has added to the pressure. Meanwhile, domestic investors supported the markets by buying shares worth ₹18,524 crore.

NIFTY50 outlook

The NIFTY50 index remains in a choppy setup after the sharp weekly fall. On the upside, 23,800-24,000 will act as the immediate resistance zone. This is the area where the index needs to reclaim strength.

On the downside, 23,550 remains the first important support. A decisive close below this level can weaken the structure further and bring 23,300-23,250 back into focus. The recent low near 23,262 will also remain an important level for traders.