On paper, it was one of India’s biggest companies by revenue. In FY26, the company reported operating revenue of nearly ₹7.8 lakh crore, up from ₹2.8 lakh crore in FY24. To understand the scale, it matches the revenue of top companies like Reliance Industries at ₹9.7 lakh crore, LIC at ₹8.9 lakh crore and Indian Oil at ₹7.6 lakh crore.

Rajesh Exports’ reported numbers placed it in the same conversation as India’s largest corporate giants. The company’s business is of gold products-importing, manufacturing, exporting, wholesaling, and retailing through Shubh Jewellers. It owned Valcambi SA, a well-known Swiss precious metals refiner.

The scale becomes even more striking because Fortune India describes Rajesh Exports as a global gold player and says it refines around 35% of the world’s total gold production. It also lists the company as India’s largest exporter of gold products

On paper, it looked like a giant. But SEBI’s interim order raises a basic question: What if the size shown to investors was not properly backed by records?

The starting point: a shareholder complaint

SEBI received a shareholder complaint in March 2024 about large trade receivables remaining outstanding for more than two years. After a preliminary review, SEBI appointed an Investigating Authority and later appointed BDO India as a forensic auditor.

In the following part, we detail the most critical allegations made.

The biggest allegation: 99.8% of consolidated revenue was overstated

This is the heart of the order. Rajesh Exports (REL) reported consolidated revenue of ₹15,44,899 crore during FY21 to FY25, which mainly came from foreign subsidiary Valcambi SA, the operating company that owns the gold refiner.

But Valcambi’s audited standalone revenue was tiny compared with the consolidated revenue that Rajesh Exports reported.

| Year (figures in ₹ crores) | Consolidated revenue of REL(A) | Revenue from subsidiaries reported by REL(B) | Actual standalone subsidiary of Valcambi SA© | Alleged misrepresentation (D=C-B) | % alleged misrepresentation |

|---|---|---|---|---|---|

| FY21 | 2,58,306 | 2,56,245 | 586 | 2,55,659 | 99.77% |

| FY22 | 2,43,128 | 2,36,891 | 729 | 2,36,163 | 99.69% |

| FY23 | 3,39,690 | 3,33,928 | 743 | 3,33,185 | 99.78% |

| FY24 | 2,80,676 | 2,75,276 | 543 | 2,74,733 | 99.80% |

| FY25 | 4,23,099 | 4,16,072 | 427 | 4,15,646 | 99.90% |

| Total | 15,44,899 | 15,18,413 | 3,027 | 15,15,385 | 99.80% |

Source: SEBI interim order on Rajesh Exports

SEBI’s prima facie view was that Rajesh Exports misrepresented ~₹15,15,385 crore of consolidated revenue, representing 99.80% of revenue.

Standalone numbers also came under question

The next major issue was at the standalone level. REL recorded huge sales and purchases with Affluence Shares and Stocks Pvt Ltd (SEBI-registered stock and commodity broker which used by Rajesh Mehta to trade in securities between FY22 and FY24), which made up around two-thirds of REL’s standalone sales and purchases over the period.

The odd part was this: REL showed huge sales and purchases with Affluence. But both numbers were almost identical. It sold around ₹11,486.60 crore and purchased around ₹11,488.42 crore. So, after doing transactions worth over ₹11,400 crore, there was hardly any value addition.

| Year (figures in ₹ crore) | Sales to Affluence | Purchases from Affluence | Difference |

|---|---|---|---|

| FY22 | 4,625.32 | 4,626.67 | -1.35 |

| FY23 | 4,934.98 | 4,935.24 | -0.26 |

| FY24 | 1,926.29 | 1,926.51 | -0.22 |

| Total | 11,486.60 | 11,488.42 | -1.82 |

Source: SEBI interim order on Rajesh Exports

SEBI’s point was simple: Why would a company do such large buy-sell transactions if it made almost no commercial gain from them?

To further compound the problem: Affluence told the regulator that REL was never its client, no agreement existed with REL, and no sale or purchase transaction was executed with or on behalf of REL. Affluence said it had trading relations only with Rajesh Mehta in his personal capacity.

SEBI further found that the transactions recorded in REL’s books broadly matched gold derivative trades done by Rajesh Mehta through his personal trading account. REL later said it wanted to trade gold digitally through MCX and, due to litigation with MCX, routed trades through Rajesh Mehta’s personal account. SEBI said this explanation was not supported by board approval, audit committee approval, authorisation, or contemporaneous records.

SEBI’s conclusion was direct: REL had prima facie misrepresented standalone financial statements by recording non-genuine sales of ₹11,486.60 crore and purchases of ₹11,488.42 crore in the name of Affluence.

Receivables: Large balances, few counterparties, unclear settlement

The original complaint was about receivables. SEBI’s findings here are important.

REL’s standalone trade receivables were heavily concentrated in four overseas entities:

| Debtor | FY22 | FY23 | FY24 |

|---|---|---|---|

| Al Jameelat Jewellery LLC (₹ crore) | 2,296.41 | 2,571.32 | 2,035.05 |

| ESG Edelmetall Handel GmbH & Co (₹ crore) | 179.23 | 200.41 | 206.69 |

| Al Sultan Jewellery LLC (₹ crore) | 286.51 | 311.4 | 120.54 |

| Aurofin SA(₹ crore) | 2,094.49 | 873.07 | 110.55 |

| Total (₹ crore) | 4,856.64 | 3,956.20 | 2,472.83 |

| % of total standalone trade receivables | 99% | 99% | 98% |

Source: SEBI interim order on Rajesh Exports

REL first said these receivables were not written off or adjusted, and that the debtors were not related to the company. Later, it said ₹2,941.13 crore had been recovered – but not through bank payments. Instead, REL claimed the dues were settled through gold supplies.

SEBI was not convinced. It said REL reduced ₹2,914 crore of old receivables through unclear set-off entries, without properly explaining how the adjustment was done, who supplied the gold, and why this was not clearly disclosed to investors.

SEBI says the company did not cooperate properly

REL did not provide (to SEBI) full access to its ERP system (accounting software), books of accounts, and journal dump. For foreign subsidiaries, it cited Swiss data protection laws and did not share primary records. Even when ledgers were provided, some details were either partly visible or missing. On sample testing done by auditor for the transactions, auditor were provided documentary proof for only handful of sample transactions.

| Sample testing | Sample size | % of transactions where complete documentation was provided to the Auditor |

|---|---|---|

| Selected transaction sample | ₹7,021.36 crore | 2.03% |

| Sales testing sample | ₹12,217.15 crore | 35.07% |

Source: SEBI interim order on Rajesh Exports

SEBI said this level of missing documentation raised serious concerns over the authenticity of the company’s financial disclosures.

Business was in subsidiaries, but investors could not see their financials

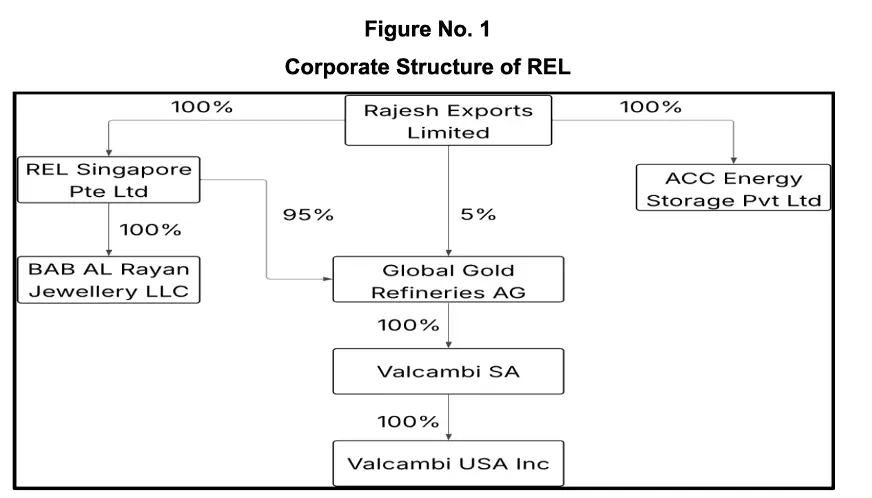

Rajesh Exports had a layered structure of multiple foreign subsidiaries:

Source: SEBI interim order on Rajesh Exports

This matters because 97-99% of REL’s consolidated revenue was coming from subsidiaries and step-down subsidiaries.

SEBI rules require listed companies to disclose separate audited financial statements of subsidiaries on their website. REL argued that investors could “derive” subsidiary numbers from standalone and consolidated accounts. SEBI rejected the argument. Consolidated accounts show one merged number. They do not reveal entity-wise risks, cash flows, receivables, payables, or related party exposure.

The “gold mines in Africa” claim was not backed by records

REL had disclosed “Other Non-Current Investments” that included an investment in gold mines in Africa.

| Claim | Amount | SEBI’s finding |

|---|---|---|

| Investment in gold mines in Africa | ₹1,035.27 crore | Unsubstantiated and unverifiable |

Source: SEBI interim order on Rajesh Exports

SEBI said REL failed to provide any entity-wise breakup, reconciliation, valuation report, financial statement reference, or supporting documentation to show the existence of these alleged investments. SEBI, therefore, found the disclosure unsubstantiated and unverifiable.

But there were other investment-related gaps, too.

In REL’s consolidated investment breakup for FY25, ₹7,745.42 crore was shown as investments recorded in Global Gold Refineries AG but GGR’s consolidated financial assets were not more than ₹10.14 crore till CY2023, creating another mismatch.

Company funds were routed through personal accounts

SEBI found substantial banking transactions between REL and Rajesh Mehta, who was the promoter, executive chairman and director.

| FY(Figures in ₹ crores) | Transfer from REL to Rajesh Mehta | Transfer from Rajesh Mehta to REL | Net |

|---|---|---|---|

| FY21 | 8.07 | 8.5 | -0.43 |

| FY22 | 180.35 | 89.46 | 90.89 |

| FY23 | 16.55 | 1.25 | 15.3 |

| FY24 | 1.01 | – | 1.01 |

| FY25 | 0.01 | 0.34 | -0.32 |

| FY26 | 132.91 | 132.9 | 0.01 |

| Total | 338.9 | 232.44 | 106.39 |

Source: SEBI interim order on Rajesh Exports

REL exchanged multiple transactions with its promoter in the name of incurring company’s expenses from the promoter’s personal account funded by the company only. SEBI said that there was no approval for routing substantial corporate funds through Rajesh Mehta’s personal bank accounts. SEBI prima facie says this seems to be case of fund diversion from the company’s books to promoters.

What SEBI has ordered

SEBI passed an interim ex parte order. The directions include:

| Direction | Details |

|---|---|

| Cooperation with the investigation | Notices must cooperate and provide documents/explanations sought by the Investigating Authority |

| Timeline for information | Certain specific information is to be provided within 30 days |

| Restriction on Rajesh Mehta | Rajesh Mehta is restrained from buying, selling or dealing in Rajesh Exports securities until further orders |

| Disclosures | REL must make true and fair disclosures of financial statements, related party transactions and other disclosures under LODR |

| New forensic auditor | SEBI directed the appointment of a new forensic auditor |

| NFRA reference | Order to be forwarded to NFRA for appropriate action, if any, against statutory auditors |

Source: SEBI interim order on Rajesh Exports

REL’s response: Denial over detail

After SEBI’s interim order, Rajesh Exports issued a press release saying the order had “no conclusive adverse findings”, that there was no fine or penalty, and that the company had done no wrong.

Technically, the order is interim. So, the findings are not final. But that does not mean the order has no adverse observations.

The larger lesson for investors

This case is not just about Rajesh Exports. It is about how investors should read large numbers.

A company can show massive consolidated revenue. But if 97-99% of that revenue comes from subsidiaries, investors need subsidiary-level clarity. If the subsidiary financials are not available, the numbers become hard to test.

A company can show large sales. But if the customer denies the transaction, there are no direct bank flows, and the trades match promoter-level derivative transactions, the sales number becomes questionable.

A company can show receivable recovery. But if the money did not come through banks and was adjusted through opaque netting, investors should ask what really happened.

SEBI’s interim order says Rajesh Exports may have presented a much stronger financial picture than the records supported. The findings are still prima facie, and the investigation is continuing. But the message is clear:

In financial statements, size is not enough. The trail behind the size matters more.