Raymond James raised Delta’s price target but downgraded the stock.

- Morgan Stanley raised its Delta price target to $115 from $105 and kept its Overweight rating.

- Raymond James raised Delta’s price target to $104 from $80 but downgraded the stock to Outperform from Strong Buy.

- The firm cited limited near-term upside after its recent rally despite strong fundamentals and continued debt reduction.

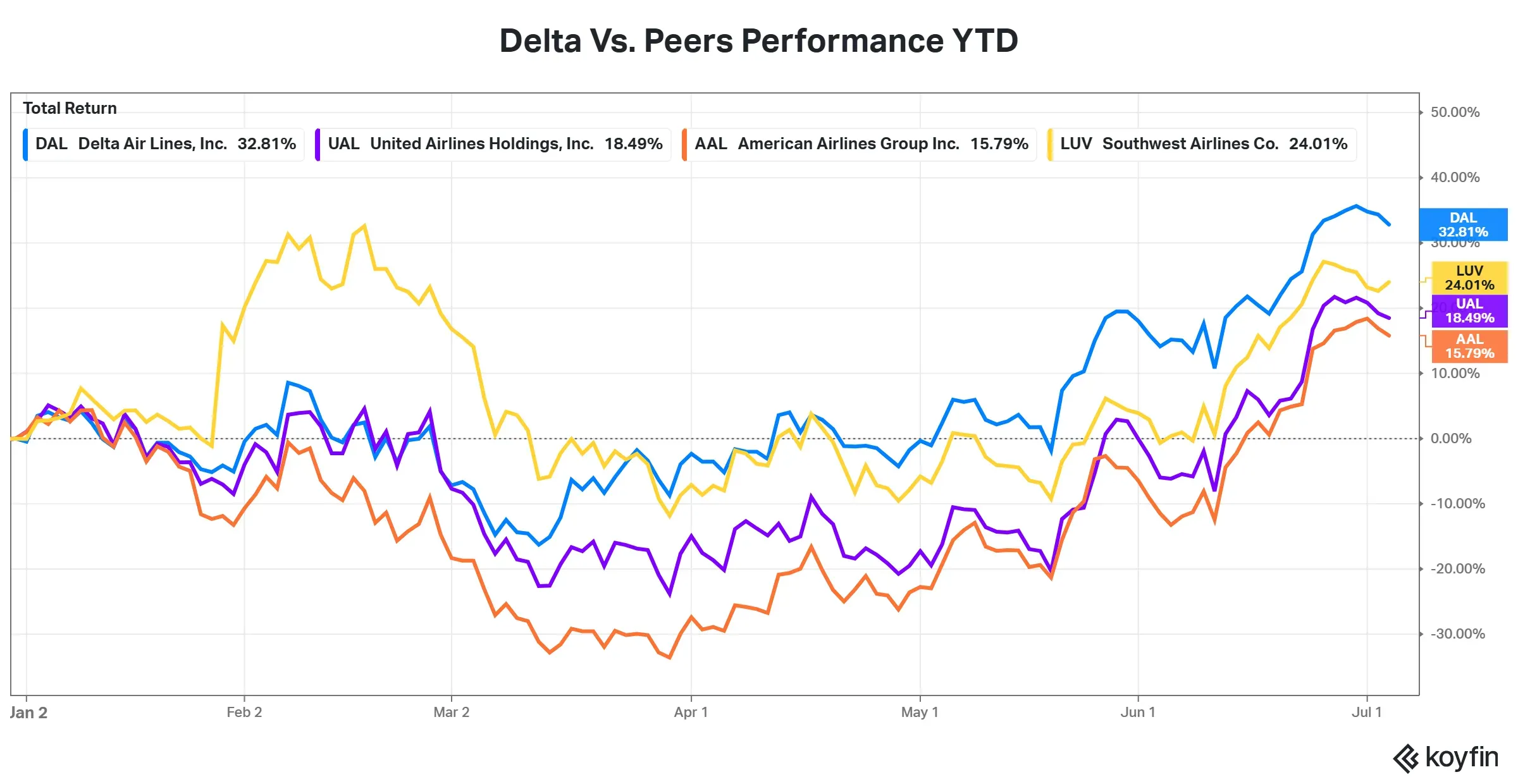

Delta Air Lines (DAL) stock slipped premarket on Tuesday and drew mixed reactions from Wall Street analysts, as the stock’s recent rally prompted debate over how much upside remains despite the airline’s favorable long-term outlook, ahead of its second-quarter earnings on Friday.

Analysts at Morgan Stanley and Raymond James both raised their price targets for Delta following their latest assessments, though they took different views on the stock’s near-term prospects.

Morgan Stanley Sees 25% Upside In Delta Airlines

Analyst Ravi Shanker increased Morgan Stanley’s price target on Delta to $115 from $105 while maintaining an ‘Overweight’ rating, implying a 25% upside to the stock’s last close.

In his note, Shanker said the second quarter, which had appeared likely to create significant operational or financial disruption, ultimately concluded on a much stronger footing than expected, reinforcing confidence in the airline’s trajectory.

Delta Air Lines’ stock edged 0.6% lower in early premarket on Tuesday.

Raymond James Turns More Cautious On DAL

Analyst Savanthi Syth of Raymond James raised the firm’s price target to $104 from $80 but lowered the stock’s rating to ‘Outperform’ from ‘Strong Buy’.

The analyst said Delta continues to stand out because of its competitive positioning, a renewed focus on its third-party maintenance, repair and overhaul business, financial strength, and disciplined capital allocation strategy.

Syth said Delta’s recent 15% dividend increase and continued debt reduction show the company is rewarding shareholders while improving its financial health.

However, the analyst also said the stock’s recent advance has narrowed the gap between its market price and perceived fair value, limiting the potential for additional gains in the near term despite the company’s solid fundamentals.

According to Fiscal AI data, analysts expect Q2 revenue of $18.78 billion and earnings of $1.49 per share.

DAL Retail Traders View

On Stocktwits, retail sentiment around the stock improved to ‘bullish’ from ‘neutral’ territory the previous day.

A user said, “oil is going to dump much lower. The airlines are in for a boom.”

Another user said, “$DAL heads into Q2 2026 earnings on July 9 with expectations already anchored by strong prior guidance. The key focus will be whether demand strength and pricing power can sustain into peak summer travel without margin compression.”

DAL stock has gained over 83% in the last 12 months.

For updates and corrections, email newsroom[at]stocktwits[dot]com.<