Indian equity markets extended their losing streak for the fifth consecutive week, marking the longest period of weekly declines since August 2025. The broader tone remained weak throughout the week, with persistent selling pressure, rising crude oil prices and macroeconomic headwinds continuing to weigh on sentiment.

NIFTY50 and SENSEX struggled to sustain any recovery, with every intraday bounce being sold into. As a result, the index ended the week at 22,819, down -1.2%, while SENSEX closed at 73,583.

A key factor behind the weakness has been the sharp spike in crude oil prices. Oil prices and a sustained decline in the Indian rupee, which slipped to a new record low of 94.96 during the week. Additionally, sustained outflows from Foreign Institutional Investors (FIIs) have further aggravated the situation. As India is a major importer of crude oil, higher prices tend to widen the current account deficit and fuel inflation concerns. This, in turn, puts pressure on the currency and equity markets.

On the sectoral front, weakness was visible across the board except for IT (+1.1%) and Pharmaceuticals (+0.1%). Defence (-4.0%), PSU Banks (-3.9%) and Real Estate (-3.7%) indices ended the week deep in the red.

Spotlight: As the Indian rupee weakens and traditional beneficiaries such as IT stocks face selling pressure, investors are gradually shifting their focus towards the pharmaceutical sector. While a weaker rupee supports export-driven revenues, the real advantage lies with companies that generate higher net foreign exchange earnings without significant import or hedging offsets. From the technical standpoint, unless index breaks the immediate support zone of 21,500 on a closing basis, it may sustain its gains at higher levels.

️Key events in focus: In U.S. the closely watched jobs report from the Bureau of Labor Statistics will be released on Friday. This could shift investor focus away from ongoing developments in the Middle East. However, the markets will not react immediately, as they will be closed on Good Friday.

Earlier in the week, key macroeconomic indicators will include the Consumer Confidence Index on Tuesday, followed by the Manufacturing Purchasing Managers’ Index from the Institute for Supply Management on Wednesday.

Meanwhile, in India, Automobile companies are set to release their wholesale dispatch numbers for March, which will be closely monitored. Experts believe steady retail demand is expected to support year-on-year improvement in volumes, offering key insights into sectoral momentum going into the new financial year.

️Crude oil: Oil prices remained volatile this week amid intensifying geopolitical tensions around the Strait of Hormuz. U.S. President Donald Trump indicated that Iran had permitted a limited number of tankers to pass through the vital shipping route. The Strait, through which nearly 20% of the world’s oil supply passes, has been at the centre of the ongoing conflict, with any disruption severely impacting global energy flows. Crude prices have surged in recent weeks amid fears of prolonged disruption. Any further escalation in tensions is likely to keep oil prices high and market volatility elevated. For the week, the U.S. Crude oil prices rose 2.3% to $102 a barrel, while the Brent Crude settled at $106 a barrel, down 3%.

Mark your calendars: The National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE) will remain closed on 31 March and 3 April on account of Mahavir Jayanti and Good Friday.

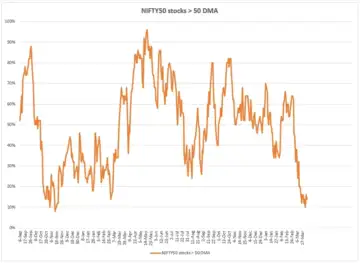

Market breadth

The breadth of the NIFTY50 index deteriorated sharply this week, with the percentage of its stocks trading above their 50-day moving average (DMA) slipping to 10-15% range, indicating widespread weakness across the index. The reading confirms that the underlying structure remains weak, with limited leadership in the market. Historically, zones below 20% tend to act as potential reversal or short-term bounce areas. However, any recovery from here is likely to be stock-specific rather than broad-based unless participation improves meaningfully above the 50% mark.

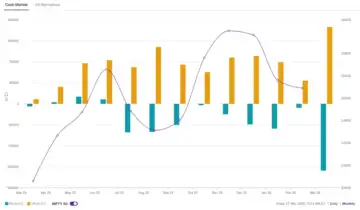

FIIs cash market and derivatives

In March 2026, Foreign institutional investors (FIIs) significantly increased their sales of Indian equities, offloading stocks worth around ₹1.11 lakh crore. This marked one of the heaviest monthly outflows on record, since September 2024.

This sustained selling has been driven by a combination of factors, including global risk-off sentiment amid escalating tensions in West Asia, a weakening rupee and rising crude oil prices. However, Domestic institutional investors (DIIs) provided strong support to the market, largely absorbing the selling pressure by purchasing shares worth ₹1.28 lakh during the month.

NIFTY 50 continues to demonstrate bearish structure, with the index closing near the lower end of its weekly range amid rising volatility and weak global market performance. Technically, the sell-on-rise trend remains in place, with immediate resistance around 23,500 and 23,850 zone.

On the downside, the index is testing a crucial support zone of around 22,450 zone. A breakdown below this range could accelerate selling towards the 22,000 level. Meanwhile, any rebound from current levels is likely to be technical in nature, unless the index decisively reclaims the 23,850 zone on a closing basis.