Even as digital lending in India is going through a transition phase with shrinking revenues for major lending apps, Mumbai-based Kissht has decided to take the plunge and go for a public issue.

Incidentally, the company is going into the IPO run with a decline in revenue in the previous fiscal year, despite operating an NBFC-led model. Consequently, there will be a lot of focus on whether Kissht’s lending business can continue to show high profitability even after the IPO.

The timing of the proposed issue is on Kissht’s side – it comes amid positive market sentiment and ahead of the DRHPs of its bigger rivals such as Navi Finserv, Fibe, and Kreditbee, all of whom are preparing for their own public listings.

Against this backdrop, we decided to take a closer look at how well-positioned Kissht is for a smooth market debut.

Backed by marquee names such as Vertex Ventures, Endiya, Alteria Capital, and cricketer Sachin Tendulkar, among others, the startup has initiated regulatory proceedings to go public after a decade of building its business in lending, which currently has about INR 4,100 Cr asset under management (AUM).

Reports doing rounds earlier this year hinted at almost an INR 2,000 Cr offering, but as per its draft papers, Kissht is raising INR 1,000 Cr in fresh funds.

From Unsecured Loans To Secured Lending

Kissht’s business empire is built on unsecured lending, the segment in which the Reserve Bank of India (RBI) increased risk weightage in November 2023, leading to a massive outcry across the lending tech ecosystem.

Paytm faced a hard time following the incident, ZestMoney shut down, while many other companies had to start pivoting or lower exposure to this segment. Even the likes of MobiKwik have seen digital lending revenue shrink and the focus has turned to other segments.

The RBI’s increased scrutiny on unsecured loans started after multiple complaints against digital lending apps, which often resorted to malpractices to recover loans from customers. Today, the industry is gradually moving towards merchant loans and secured loans.

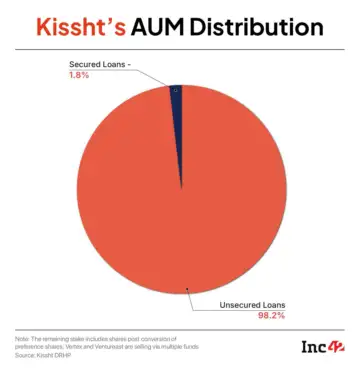

However, Kissht’s unsecured personal lending today contributes to 98% of its AUM (as of FY25). This explains the revenue shrinking to some extent.

The company aims to channelise INR 750 Cr from the IPO proceeds to augment the capital base Si Creva, which is Kissht’s NBFC arm. Personal loans are disbursed through Si Creva, which alone comprises more than 60% of Kissht’s total AUM, and other NBFC partners.

Besides personal loans, Kissht has added secured loans through loans against property (LAP) in the Q4 FY24, but this contributed to less than 2% to its total AUM in FY25.

Kissht has a hybrid model offering a physical experience and currently offers LAP through 62 branches across six states and one union territory.

While it is quite clear that Kissht is trying to make a transition from unsecured to secured lending space, which would be critical for the company’s future growth, it continues to have a significant exposure to the unsecured loans segment.

Third-party NBFCs comprise 39.4% of Kissht’s AUM currently, but going forward, Kissht would want to reduce this share and earn more by directly lending through Si Creva, where it is looking to pump a majority of the funds raised in the IPO.

There are two red flags at Si Creva, though, including an Enforcement Directorate (ED) notice from 2023 and a previous classification of the entity as a ‘High Risk Financial Institution’ by the Financial Intelligence Unit of the central government. It’s not clear whether the NBFC has steered clear of these compliance and potential legal roadblocks.

What’s Hurting Kissht’s Profitability?

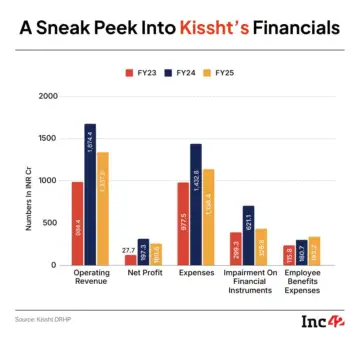

Despite a slowdown in the unsecured lending space, Kissht AUM via its NBFC continued to grow. As per its DRHP, Si Creva sanctioned loans worth INR 252.4 Cr in the last financial year (FY25), which grew 68% year-on-year (YoY).

However, its total AUM growth slowed to 56.92% YoY in FY25 compared to 105% YoY in the previous year.

As of March 31, 2025, the company acquired 53.23 Mn registered users and served 9.16 Mn customers. However, Kissht’s earnings have diminished in the last fiscal year.

Its operating revenue fell over 20% to INR 1,337.47 Cr in FY25 from INR 1,674.45 Cr in FY24 as the income from interest on loans crashed.

As a result, the bottom line also took a hit. Kissht’s net profit was down 18.6% to INR 160.62 Cr in FY25 from 197.29 Cr in the previous fiscal year.

After growing 70% YoY in terms of revenue in FY24 and a whopping 613% YoY growth in profits, this was a disappointing fiscal year for the company.

Kissht has directly cited its AUM growth slowdown for the revenue decline. From short-term lending at high interest rates, which are usually huge revenue drivers, it is moving to longer tenured loans.

“Now that the company is switching and changing that business model, from short-term loans to digital LAP, its revenue has taken a hit,” said a digital lending startup exec requesting anonymity, given Kissht’s DRHP is now under regulatory scrutiny.

What is worrisome is that profits have plummeted just as much as the revenue. In this context, it’s also pertinent to note that Kissht’s write-offs have also increased. It wrote off INR 438 Cr of financial assets in the last fiscal, which rose from INR 349 Cr in FY24 and INR 258 Cr in FY23.

The company’s expected credit loss against standard assets stood at INR 165 Cr in FY25, and net cash flow worsened to a negative INR 661.4 Cr from negative INR 637.4 Cr in FY24.

As a BFSI company, Kissht would need to show solid and robust fundamentals to stand out for investors. Positive cash flow is a highly important metric, and here Kissht needs to do a lot of work to prove to investors that it can turn things around.

If and when the company releases its pre-IPO RHP after the SEBI approval, these questions will be answered to a certain extent as that would include further disclosures.

The Digital Lending Red Flags

There are multiple areas where Kissht might stumble in its path to going public, besides its income slowdown. This includes the case led by ED under the Prevention of Money Laundering Act as well as other red flags in its NBFC business.

While Kissht said that it has not received any further communications from the ED since submitting the responses, it also mentioned that there are possibilities of future inquiries into the matter, which “could escalate to investigations, legal proceedings or any possible penalties”.

For companies that are regulated entities under the RBI, checks and balances are done by two regulatory authorities: SEBI and RBI, before they get listed. In fact, Kissht has clearly disclosed that it is exposed to regular inspection by the central bank.

Ayush Mohata, partner of capital markets team at Khaitan & Co, said that in such instances, SEBI typically always writes to the relevant sectoral regulator (RBI in this case) to seek their feedback/concerns on the IPO-bound entities, and to check whether there are any outstanding regulatory actions or investigations pending pertaining to the entity and connected persons, before the market regulator gives clearance for the IPO.

Meanwhile, Kissht also operates in a very risky area where it has to walk the tight rope of acquiring and retaining customers in a highly competitive lending market while abiding by the legal and ethical practices.

Whether it’s Kissht or other lending players, it’s not a hidden secret that these companies often embrace dark patterns in customer acquisition and loan recovery processes. From Reddit to X, there are hoards of user complaints even today against Kissht pointing at recurrent user harassment.

In fact, in 2020, the Andhra Pradesh Police and Crime Investigation Department (CID) deemed Kissht, among 29 others including Easy Loan, Fortune Bag, Rupee Loan, Udhaar Loan, Robo Cash, CashTM, Quick Cash, as ‘problematic’ for multiple complaints related to user harassment.

In 2023, Kissht was also among the 94 loan apps banned that were banned by the Ministry of Electronics and Information Technology (MeitY) for alleged China links, which was revoked after a few months.

Clearly, Kissht and some of its new-age competitors have repeatedly come under the scanner for their alleged association with illegal activities. Despite that, India’s digital lending market has boomed over the last few year and continues to grow, Kissht has continued to raise funding (more than $140 Mn raised in total), roped in a celebrity figure like Sachin Tendulkar as investor and brand ambassador in 2024, and is now headed for the public market.

Will Kissht Convince Investors?

Despite the above risks and operational challenges, it goes without saying that Kissht operates in a lucrative market. Inc42’s report suggests that the country’s digital lending opportunity will reach $1.3 Tn by 2030 from $402 Bn in 2024, comprising 60% of the total fintech market.

As per another report, as mentioned in Kissht’s DRHP, digital lending within the mass market segment is projected to surge 7X to INR 4,100 Cr by FY30, growing at a 48% CAGR from FY25, outdoing the growth of conventional players.

In fact, though there are legacy competitors like Bajaj Finserv, Cholamandalam, HBD Financial Services, among others, with much higher AUM and revenue compared to Kissht, the latter’s AUM growth rate between FY23-25 has been higher than the rest.

However, the real major competition the company faces is from the other new-age players like Kreditbee (which crossed INR 2,000 Cr in revenue while profit jumped 66% in FY25), Fibe (which has much lower interest rates compared to Kissht and also offers loans to salaried professionals), and Navi Finserv (also has higher revenue compared to Kissht).

“Kissht’s IPO sets the stage for bigger NBFCs and digital lending players that are also mulling their IPOs in the coming months. If the market is ready for a mid-sized IPO like this, by the time it’s listed, I think the large mutual funds and other public market investors will have more confidence for the next level and bigger players coming in,” said the founder at another IPO-bound digital lending platform, requesting anonymity, citing the sensitivity of the matter.

For instance, last year, a large number of NBFCs started getting listed. Following that surge, when HDB’s IPO happened, there was no dearth of subscriptions despite it being one of India’s largest IPOs so far. However, there seems to be a sudden change in the NBFC IPO trajectory after a sudden surge.

Sourav Choudhary, MD at Raghunath Capital, noted that NBFC IPOs are taking a turn: from euphoria to selectivity.

“The market mood has cooled, but this is less a slowdown and more a shift towards quality. Investors are now looking beyond growth stories, focusing on balance sheet strength, governance, and sustainability.”

Choudhary also believed that Kissht’s DRHP filing captures this change. “The company has built a strong digital lending platform, but with slowing disbursements and softer profits, the IPO will test how fintech-NBFCs are valued in today’s more discerning market.”

For now, the decision is on SEBI. But, as the public market investors get selective, and scale, governance and fundamentals continue to command better demand, Kissht has a lot more to do to convince investors.