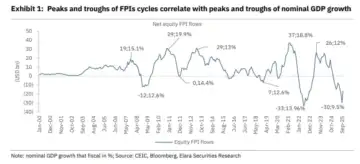

After almost a year of capital outflows from foreign portfolio investors (FPI), India seems poised for a notable recovery. A recent report from Elara Capital, which has tracked FPI trends for the last 15 years, shows that foreign investments largely depend on one crucial factor, which is nominal GDP growth.

Experts believe that this growth is expected to pick up speed by FY27-28, potentially triggering a revival in FPI inflows as early as the first quarter of 2026.

“The key factor influencing FPI appetite for Indian equities is nominal GDP growth, which has historically shown a strong correlation with FPI inflow cycles. Five peak-to-trough FPI cycles since 2010 align closely with India’s nominal GDP cycles,” said Elara Capital in its report.

Additionally, the brokerage firm noted that a considerable portion of foreign portfolio investment outflow has been linked to the absence of dedicated AI opportunities in India and increasing geopolitical tensions.

The brokerage firm also highlighted that the primary factors contributing to FPI outflows since 2024 have been sluggish growth, even though the weakness of the DXY has provided some support. Consequently, a shift in domestic growth trends should promote FPI inflows, as valuations have become more attractive and the outlook for the USD (DXY Index) remains favourable.

“We expect India’s growth drivers to turn incrementally supportive, with nominal GDP growth expected to recover to 10% in FY27E from ~8% in FY26E. The real GDP would however be 7% for both years,” said Elara Capital.

Check out 4 key triggers for FPI to turn positive into Indian market

India’s policy mix has become growth supportive

The brokerage firm indicated that the supportive fiscal policy aimed at reducing personal income tax and GST is conducive to economic growth. While the intertemporal effects of pent-up demand resulting from GST reductions are crucial to monitor, initial signs at the onset of a seasonally robust Q3 imply that consumers are beginning to spend (PFCE constitutes 55-60% of GDP).

Elara Capital said the furthermore, public capital expenditure has gained momentum at both the central and state levels, which has the potential to generate sustainable growth impulses.

Trade deal with the US near

Elara Capital noted that the implementation of tariffs by the US significantly contributed to the unfavorable outlook on Indian asset classes. Recent updates regarding India-US trade agreements are encouraging, and we maintain our position that a trade deal could be achievable in 2025.

“We expect Russia oil import-related 25% tariff to be retracted. If materialized, we see policy implied effective tariff rate on India at 17-18% versus 32-33% currently. As a base case, we expect 10% baseline tariff and Section 232 tariffs to stay, leading to an effective tariff rate of 9-10%,” said Elara Capital in its report.

Accommodative monetary policy

The brokerage firm stated that globally, the Federal Reserve has resumed its cycle of rate cuts, which is expected to benefit emerging markets (EMs). Anticipation of these rate reductions from the Fed has led to a decline in US rates, with the two-year yields falling approximately 82 basis points and the 10-year yields decreasing around 70 basis points from their highs year-to-date (CYTD).

As per Elara Capital, the US Dollar Index (DXY) remains stable within the 95-100 range, aligning with our forecasts after experiencing an 8.5-9% drop so far this year. The combination of lower US yields and a weaker US Dollar, coupled with the Federal Reserve’s shift to a more accommodative stance, has created an ideal environment for emerging markets to implement supportive monetary policies aimed at fostering growth.

“Domestically, benign inflation and nominal growth have created ample policy space for the RBI MPC to undertake 50bps rate cut in the next two meets in FY26,” said the brokerage.

Earnings outlook improving

According to Elara Strategy, this quarter (Q2FY26) signifies the beginning of a new earnings upcycle, with PAT anticipated to increase by 12.5% year-over-year, marking the first occurrence of double-digit growth in six quarters.

While the incremental earnings for FY26 are primarily focused on commodity-driven sectors, we predict that the growth in FY27 will be more widespread as consumption and industrial recovery gain momentum. Among the 179 companies covered by Elara that have reported thus far, there has been an 8% year-over-year increase in sales, a 15% rise in EBITDA, and a 16% increase in PAT.

With approximately 30% of the results still outstanding (as of November 13), the brokerage expects these figures to remain consistent throughout the entire result cycle. In their evaluation, 73 out of the 179 stocks have reported results exceeding expectations, while just 39 have fallen below estimates – indicating roughly two beats for every miss.