The practical benefit here is decision clarity. A buyer who knows they qualify for a loan at a specific rate and EMI for a specific car can make a purchase decision with full information.

Most buyers who are familiar with new car finance assume that used car finance works the same way. The broad structure is similar: a lender advances the money, the buyer repays it in equated monthly instalments, and the car is hypothecated to the lender until the loan is fully repaid. But the specific terms, eligibility criteria, and risk factors in used car finance are meaningfully different from new car loans, and understanding those differences before applying can save a significant amount of money over the loan tenure.

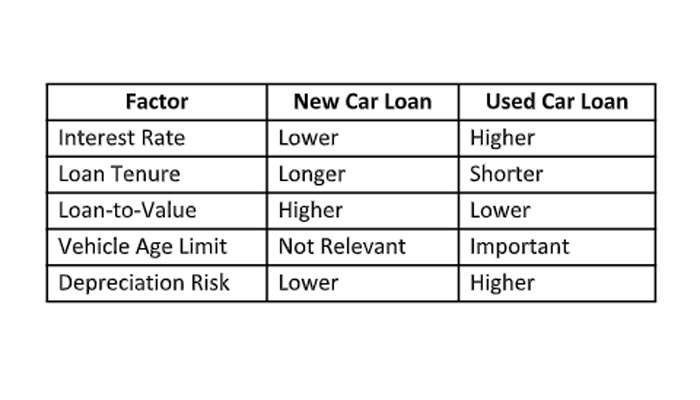

Used Car Loan vs New Car Loan: The Differences

The most immediate difference is the vehicle age constraint. New car lenders are advancing money against a vehicle that will depreciate, but is at peak value at the time of purchase. Used car lenders are advancing money against a vehicle that has already depreciated and whose residual value is more difficult to assess. This affects both the maximum loan amount available relative to car value and the maximum tenure that lenders will extend.

A second important difference is the interest rate. Used car loan rates are typically higher than new car loan rates, reflecting the higher uncertainty around collateral value. For the same loan amount, this difference in rate can meaningfully affect the total repayment cost over a three to five-year tenure.

How Loan Eligibility Is Calculated for a Used Car

Used car loan eligibility is assessed on two dimensions simultaneously: the creditworthiness of the borrower and the overall value of the vehicle. Both must pass the lender’s standards for a loan to be approved at the requested amount.

Borrower creditworthiness is assessed through credit score, income documentation, existing EMI obligations, employment stability, and residential stability. A credit score above 750 typically qualifies a borrower for better interest rates. Scores below 650 may lead to rejection or to significantly higher rates. Income documentation requirements also vary by employment type: salaried applicants typically provide salary slips and bank statements, while self-employed applicants provide income tax returns and business bank statements.

Coming to vehicle value, the financials are assessed based on the car’s age, condition, variant, and market value. Most lenders apply a Loan to Value ratio that limits the loan amount to a percentage of the car’s assessed value, typically between 80 and 90 % for newer used cars, declining as the vehicle ages. This is why the age of the car significantly affects how much can be borrowed against it.

The intersection of these two assessments determines both eligibility and amount. A buyer with strong credit applying for a loan on a five-year-old, well-maintained car will receive different terms than a buyer with moderate credit applying for a loan on a nine-year-old car at its maximum eligible age.

Vehicle Age Limits and Why They Affect Your Loan Terms

Most lenders cap used car loan eligibility at a maximum vehicle age at the end of tenure. If a lender’s policy is that the car must not exceed 12 years of age by the time the loan is repaid, and the car is already eight years old, the maximum tenure available is four years. This directly determines the minimum EMI, since a shorter tenure means higher monthly payments.

Older vehicles also attract lower maximum Loan to Value ratios because their residual value at the end of a multi-year loan tenure is difficult to predict. A car that is seven years old today will be twelve years old at the end of a five-year loan. At that age, the car’s market value may be a fraction of the original loan amount, which increases the lender’s risk.

For buyers who are considering vehicles that are already seven to ten years old, these age constraints mean that large loan amounts may not be available, and shorter tenures will produce higher EMI obligations. Understanding this before selecting a car prevents the situation where a buyer falls in love with a car, applies for finance, and discovers that the loan terms make the monthly payment unaffordable.

How EMI Changes With Tenure and Why Total Cost Matters More

The EMI is the monthly payment that a buyer sees when they evaluate affordability. But EMI is only one dimension of the loan cost. The total repayment, which is the EMI multiplied by the number of months, is the number that actually represents what the car costs, including finance.

A loan of five lakh rupees at 16% interest rate repaid over three years generates a different total repayment than the same loan repaid over five years. The longer tenure produces a lower monthly EMI, which looks more affordable month to month, but generates significantly more interest over the life of the loan.

The difference is not trivial. On a five lakh loan at 16% interest rate, the difference in total interest paid between a three-year and a five-year tenure can exceed forty thousand rupees. For a buyer who is choosing between a three-year and five-year tenure based on which monthly payment fits their budget, the total cost difference should be part of the comparison.

Processing fees, documentation charges, and foreclosure penalties add further layers to the actual cost of a loan. Some lenders charge a flat processing fee. Others charge a percentage of the loan amount. Foreclosure penalties, which apply if the loan is repaid early, can be significant for buyers who expect to sell the car before the tenure ends.

Why Finance Approval Should Be Integrated Into the Buying Journey

One of the common frustrations in used car buying is the time gap between finding a suitable car and confirming that finance has been approved at acceptable terms. In informal transactions through local dealers, buyers sometimes put down token payments before their loan eligibility or the car’s eligibility for a loan has been confirmed. If the loan is not approved, or is approved at terms that make the purchase unaffordable, recovering the token payment can be complicated.

An integrated finance process, where loan eligibility and terms are assessed as part of the same transaction flow as the car selection, eliminates this uncertainty. When buying from organised used car platforms like Cars24, an integrated financing process is accessible from the platform itself. This means a buyer can understand their loan eligibility, interest rate, and EMI before committing to a purchase, rather than discovering terms after a token amount has been placed.

The practical benefit here is decision clarity. A buyer who knows they qualify for a loan at a specific rate and EMI for a specific car can make a purchase decision with full information. A buyer who discovers post-commitment that the loan terms are different from what they expected has fewer options.

How to Avoid Over-Borrowing on a Used Car

The maximum loan amount available for a used car purchase does not represent what a buyer should borrow. Lenders set eligibility limits based on their assessment of the ability to repay. Buyers should set their own limit based on the total cost of ownership, including EMI, maintenance, insurance, fuel, and any other fixed expenses associated with car ownership.

A useful approach is to calculate the maximum monthly payment that is genuinely comfortable rather than merely technically manageable. The difference matters because car ownership comes with variable costs. A month that involves a service, an unexpected tyre replacement, and an insurance renewal on top of the EMI is financially different from a quiet month. The EMI should be set at a level that leaves room for these fluctuations without creating financial stress.

Down payment decisions also affect long-term cost. A higher down payment reduces the loan amount, which reduces total interest paid and produces a lower EMI. For buyers who have the flexibility to put down a larger initial payment, the long-term savings are real. Utilising intuitive EMI calculators by platforms like Cars24 allows buyers to model different combinations of loan amount, tenure, and down payment to find the right structure before applying.