AT&T reported quarterly results that topped earnings expectations but missed Wall Street’s revenue estimates.

- In an interview with CNBC, AT&T CEO John Stankey said satellite competitors are entering the market do not currently address a meaningful gap in AT&T’s coverage.

- The CEO also said AT&T has no immediate need for a dedicated satellite partner, though it remains open to working with multiple providers when appropriate.

- Retail traders on Stocktwits questioned whether analysts who recently cut price targets over Starlink concerns would now reverse those views.

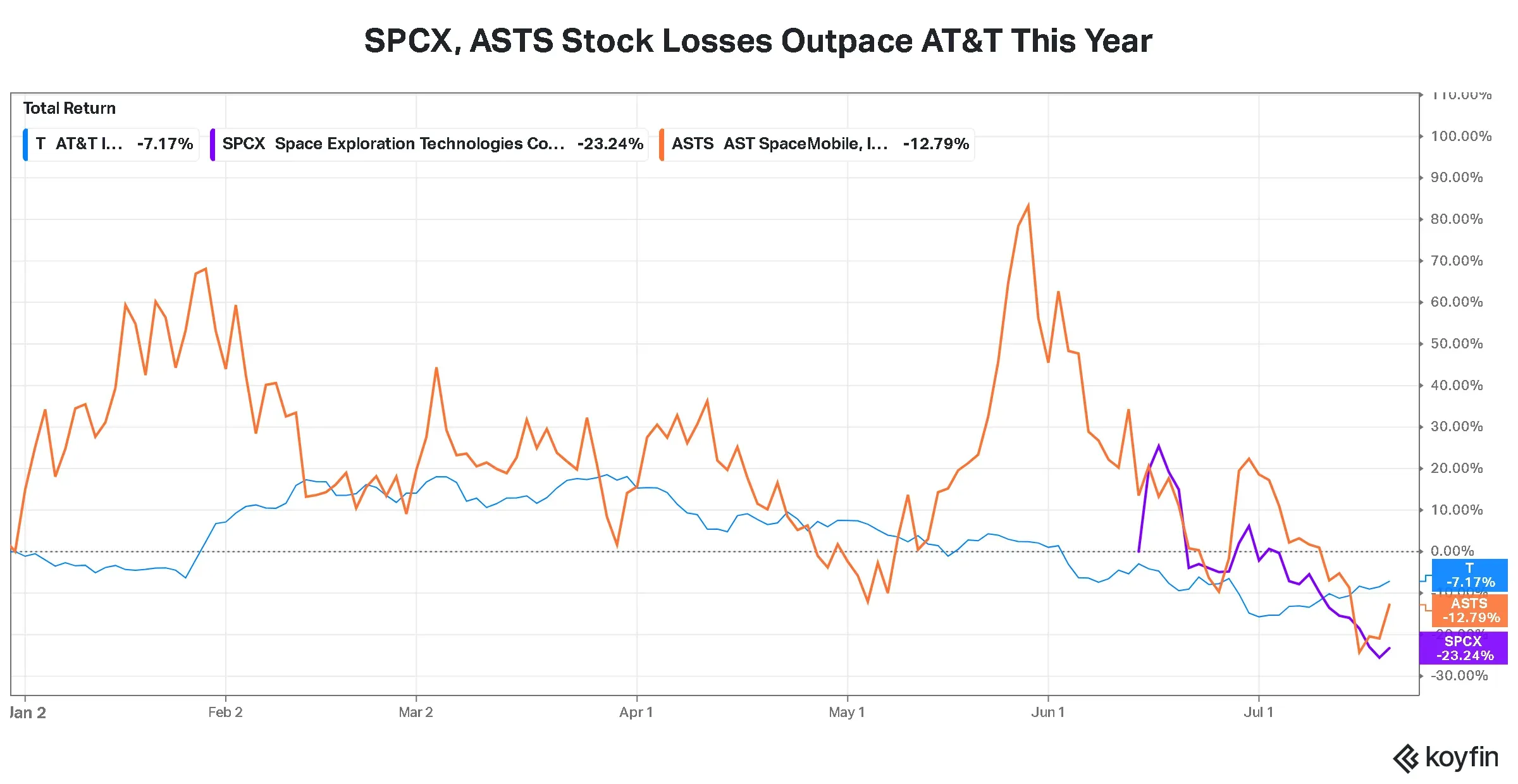

AT&T (T) shares rose in early morning trade on Wednesday after the company beat earnings expectations, giving CEO John Stankey a strong backdrop to push back forcefully against Wall Street’s biggest lingering worry about the stock: competition from SpaceX’s (SPCX) Starlink.

In an interview with CNBC, Stankey dismissed Wall Street concerns about competition stemming from Elon Musk-led Starlink. “There are going to be new competitors, and there are going to be folks that come in. But the reality is that they’re coming to the game very late after this industry has been established. They have to catch up with substantial amounts of infrastructure investment that’s been going on for decades,” he said.

His comments came after AT&T reported quarterly results that topped earnings expectations, but missed on revenue forecasts.

T’s stock rose 4.3% in pre-market trade and was among the top trending tickers on Stocktwits at the time of writing. Retail sentiment around the company improved to ‘neutral’ from ‘bearish’ territory over the past day, and chatter rose to ‘normal’ from ‘low’ levels. Platform data showed an over 180% jump in message volume in the last 24 hours.

CEO Says AT&T Doesn’t Need Starlink

In the CNBC interview, Stankey also addressed speculation over whether AT&T could eventually partner with Starlink through a wholesale agreement.

He said the company doesn’t currently see a need for satellite service as a core part of its distribution strategy because AT&T already handles more than 98% of traffic across its converged customer network.

“I don’t feel a need right now that I need to have a satellite partner as a main distribution vehicle for me because I don’t think it addresses a part of the market that I can’t get to on my own,” he said.

The trigger came June 26, when the Financial Times reported that SpaceX president Gwynne Shotwell told IPO roadshow investors that SpaceX intends to launch a Starlink-branded retail mobile service for U.S. consumers, potentially building its own terrestrial wireless network, reframing Starlink from a carrier partner into a direct competitor for AT&T’s more than 109 million mobile subscribers.

Is Musk Or Jassy A Better Fit For AT&T?

When asked whether AT&T would prefer to work with Elon Musk’s Starlink or Amazon (AMZN)-backed satellite services if needed, Stankey rejected the idea of choosing a single provider.

Instead, he pointed to the joint venture AT&T formed with Verizon (VZ) and T-Mobile (TMUS), saying it allows the carriers to work with multiple satellite operators, including SpaceX, Amazon and AST SpaceMobile (ASTS), for the small percentage of coverage that falls outside their terrestrial networks.

AT&T EPS Tops Estimates, Revenue Misses

AT&T reported earnings per share of $0.65, ahead of Wall Street expectations of $0.59, according to Koyfin. Revenue came in at $31.6 billion, slightly below analysts’ consensus estimate of $31.8 billion.

The company added more than one million strategic customer accounts, its strongest pace in three years, alongside nearly 370,000 fiber subscribers and 430,000 postpaid wireless subscribers.

Retail Traders Push Back On Starlink Narrative

Many retail investors on Stocktwits argued that the market had overstated the competitive threat from Starlink in recent weeks. One trader questioned whether analysts who cut price targets over satellite competition would now reverse those calls following Stankey’s comments and the company’s results.

View this Stocktwits post

Another said the quarter could help ease investor concerns that Starlink would significantly disrupt the U.S. wireless market, which continues to be dominated by AT&T and its larger telecom peers.

View this Stocktwits post

After SpaceX president Gwynne Shotwell told IPO roadshow investors that SpaceX intends to launch a Starlink-branded retail mobile service for U.S. consumers in June, a slew of commentary from Wall Street followed. Oppenheimer downgraded AT&T to ‘Perform’ from ‘Outperform’, warning that low-earth-orbit satellite constellations pose a structural threat to the company’s broadband and mobile subscriber growth.

Earlier this month, Wells Fargo initiated coverage of T’s stock with an ‘Underweight’ rating and an $18 price target, implying nearly 15% downside, with analyst Steven Cahall writing that “outside of T’s fiber footprint we think competition will be fierce” and that AT&T’s wireless additions look “most at-risk.” Morgan Stanley also cut its price target to $25 from $30 earlier this month, but kept an ‘Overweight’ rating on AT&T shares, noting that “the fear of the unknown has led many to shoot first and ask questions later in Telecom.”

While satellite connectivity remains an emerging competitive force, AT&T’s CEO views it as a complementary technology for hard-to-reach areas rather than a replacement for decades of investment in terrestrial wireless and fiber infrastructure.

Read also: GEV Stock Drops On Q2 Earnings Miss – CEO Raises Guidance, Says Data Center Orders Have Already Doubled 2025 Total

For updates and corrections, email newsroom[at]stocktwits[dot]com<